What is the F.I.R.E. Movement??

Please forgive any mistakes in my English—I’m still learning and appreciate your understanding.

This article begins in a completely conventional and expected way, with a definition of what the title announces.

F.I.R.E. is an acronym that stands for “Financial Independence, Retire Early,” a movement that advocates saving as much as possible (I’ll delve deeper into this; it’s not as absolute as it might seem, as you’ll read in a few lines) in order to stop working at a relatively young age. Breaking it down into phases, it involves creating a spending plan, analyzing all the monthly expenses, and cutting unnecessary costs. By doing so, it will be possible (and necessary) to save significantly, invest the savings, primarily in long-term plans, and – when the invested amount reaches a reasonable level (again, I’ll go into more detail in a few lines) – you can stop working actively.

How I Started

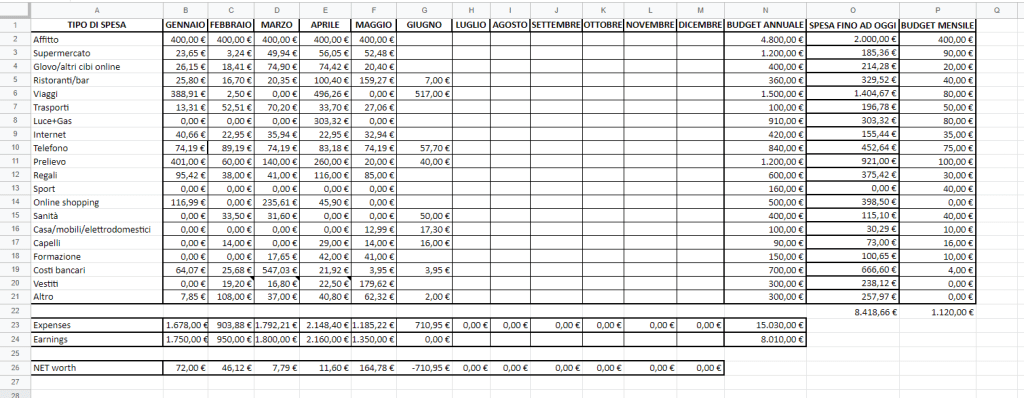

In my personal case, it always begins with setting up an Excel or Google Sheet (or whatever tool you prefer, as long as it allows for quick calculations and can be updated in a relatively short time) where you can record all expenses incurred up to that point.

For example: On June 10, 2022, I decided to start tracking my expenses to avoid waste. I logged into my bank’s website and, under the transaction history section, I found all the transactions that occurred from January 1, 2022, to June 10, 2022. I then set up a Google Sheet where I listed the types of expenses in the rows (e.g., coffee shop, restaurant, entertainment, shopping, etc.), and the months in the columns. The next step was to enter how much I spent each month under the corresponding category. Once this was done (it took me about two hours since I had already prepared the file beforehand), I had a clear monthly breakdown for each expense category. At this point, identifying unnecessary expenses and waste was incredibly easy. Once you reach this stage (referred to as “Money Awareness”), cutting the superfluous and choosing to forgo certain expenses becomes a purely subjective and personal decision. However, the awareness this exercise provides offers a benefit that has no monetary value: the power of choice. [My advice is always to make sure you feel comfortable; there’s no point in cutting out the TV, computer, and other items to be financially satisfied but personally unfulfilled—the challenge is finding a balance between what you need to feel good and what you can eliminate without too much discomfort.] Once you have prepared your expense tracking sheet, you will see a clear monthly amount that, after eliminating the superfluous, is needed to live a balanced life (calculate the average total monthly expense). This will be your reference budget. You have just created a BUDGETING plan, which you will need to adhere to almost scrupulously if you want tangible results (at least for the first few months, to allow your mind and lifestyle to get used to the idea of having a limit that didn’t exist before). Here’s an example:

Step 1: The beginning of my career and first earnings

Let’s consider “mediocre”—just for the sake of having a reference point—a monthly salary of €1,000 in Italy in 2023. In this case, in my opinion, it’s still necessary to set up a spending plan to minimize expenses. My entry into the job market wasn’t ideal: I learned the hard way that a recent graduate in Italy earns between €600 and €950 per month. The first firm I worked for offered me a gross monthly salary of €950 (along with the offer, I had to open a VAT number) for eleven months; August, of course, meant “vacation” but also “office closed,” and who pays someone who isn’t coming into the office to work? Nonetheless, it was enough for me to live in a small, cold attic apartment in a big city, buy the essentials, and get by during my first year. Later, I switched firms, got a raise, moved to a better apartment, and things improved. It’s crucial, especially with low incomes, to understand where your money goes. In a situation of low earnings, such as in your early twenties, it’s essential to create personal value that the market will pay for (and hopefully pay well). Learning skills, getting training, and expanding your work experience are necessary and extremely important if you don’t have a substantial income. Acquiring a soft skill is crucial in this day and age, even just to earn a moderate income; the demand for specific and complex knowledge is the foundation of today’s job market—just think of how many competencies and certifications are required to even apply for most jobs. However, even without an acceptable income, it’s important to understand that the principle behind the F.I.R.E. movement is incredibly useful for learning how to manage your finances. It’s astonishing that there isn’t mandatory basic education on financial management nowadays, and even more astonishing how much ignorance there is in this field. Most people have no idea where the money they sweat for five (or even six) days a week goes, trading precious time for something they don’t even know what happens to; the only certainty is that by the end of the month, the fruit of that labor is completely gone. For this reason, I consider it imperative to track my expenses and be aware of what I’m buying with my time.

Step 2: Maximizing

I always enjoy challenging myself. There have been times in my life when I’ve literally thrown money away for the sake of social proof, which, as I later realized, was pointless. I’ve also gone through periods where I tried to spend as little as possible, managing my finances almost obsessively, and I was surprised to discover just how accustomed we are to the superfluous in our daily lives. I refer to the periods when I test my spending limits as being “ON FIRE.” During these periods, I aim to reduce costs and maximize income as much as possible; in the past, I’ve asked for raises or tried to maximize the earnings from a side hustle. It can be useful to work overtime or perhaps learn a new skill; recently, I’ve been focusing on acquiring the knowledge needed to become a Certified Public Accountant, for example. At the same time, I usually lower my lifestyle standards, avoid buying coffee at the café (leading to a catastrophic decline in my social proof, but that’s life), avoid restaurants, look for cheaper alternatives to Spotify, seek better deals for electricity and gas—in short, I “tighten the belt.” In particular, I never would have noticed that I was spending about €300 each month on cafés and restaurants, which can easily be avoided for a period of time; taking this opportunity, I also quit drinking coffee (current streak: two months and seventeen days). It’s amusing to realize that everyone drinks coffee at the café to “feel awake” without ever trying to go without it for a few weeks; since I quit, aside from the first week of incessant headaches, I feel much more alert and active. I’m still only twenty-eight and not yet fully settled on my future, so the only thing I can do is accumulate, without a defined goal, but for two main purposes:

- Investing a significant amount long-term to free myself from complete dependence on work.

- Creating an ever-growing cushion to handle daily crises or negative events;

Step 3: Protection and Investment

The first piece of advice I would give is to create an emergency “cushion”; personally, I consider it necessary to accumulate an amount in your bank account equivalent to at least four months of expenses for your lifestyle. For example, if your monthly expenses that keep you comfortable are €1,000, you should aim to build a cushion of at least €4,000. Some authors suggest six to eight months, while other schools of thought (more “YOLO”-oriented) suggest two months. I feel “safe” with four months: this fund serves as a “lifesaver” in case of unexpected expenses (e.g., an unexpected cavity, hospital stay, broken washing machine, etc.). It’s a good practice to increase the cushion year by year to combat inflation: if your personal lifestyle costs €1,000 per month in the initial reference year, you can accumulate a minimum cushion of €4,000, but if after a few years your lifestyle costs increase to €2,000 per month, the cushion should be increased to €8,000 (it seems obvious, but it isn’t). Once you’ve accumulated your emergency cushion, you can finally focus on investments. In my personal experience, after surpassing a threshold I consider important, I sought the help of an independent advisor, and together we created an optimal portfolio. This choice is very subjective. Entrusting your assets to a third party definitely has its pros and cons; here are some that I’ve identified (but there are certainly many more):

PROS

- From the advisor’s perspective, managing someone else’s wealth ensures decisions are made without emotional bias, leading to objective investments.

- A second perspective can make a real difference; often, a self-taught individual’s view is shortsighted and limited to the content they were trained on. A second opinion can expand the range of choices and knowledge.

- Having an advisor will certainly provide constant updates on your financial situation.

CONS

- Any advisor comes at a cost. The market offers both more expensive and less expensive advisors, but the cost doesn’t necessarily correlate with expertise. Some advisors charge a fee based on a percentage of the invested amount. In my opinion, the range worth considering is between 0% (unrealistically low) and 1%. In this model, the advisor is incentivized to maximize investment profits because they will receive a higher fee as a result. Other advisors prefer a fixed payment method, unrelated to the value of the investment; in this case, it’s unclear what their incentive is to increase client profits (there’s an underlying but important component here: “good faith”). If you have no knowledge of investing and want to start learning, I recommend reading “The Intelligent Investor” by Benjamin Graham (unfortunately, Amazon doesn’t pay me any commission for this recommendation).

Step 4. Ongoing.

When the 2-3% annual return on your invested capital covers a year’s worth of expenses, you can consider yourself in F.I.R.E. territory. With such an amount invested, withdrawing 2-3% each year will allow you to live off the returns without depleting the principal. When I first heard about F.I.R.E.—I’m young, so we’re talking about five or six years ago—I read everywhere that you needed an amount where 4% could cover your annual expenses. However, today, much to my dismay, more and more experts base their calculations on a figure that doesn’t exceed Pi (like Mr. Rip, for example—he doesn’t pay me a commission for the mention either, but he’s an influential figure in the Italian finance landscape). There’s a significant difference between the previous and current values, even though it might seem like a minor change. After all the preliminary preparation, at this point, I can only wish you a happy personal and financial journey, where the ultimate goal/the final chimera is always freedom.

P.S. None of the parts of this article should be considered financial advice, even though there’s no specific detail about any product: it’s simply the story of my experience with investments.

P.P.S. I recommend finding a balance between your personal and professional life, where you can earn well but also ensure peace of mind (or whatever else will be clarified later). This is a separate issue that is particularly close to my heart, and I’ll write an article about it in the future.

Which step are you on? Let’s discuss in the comments.